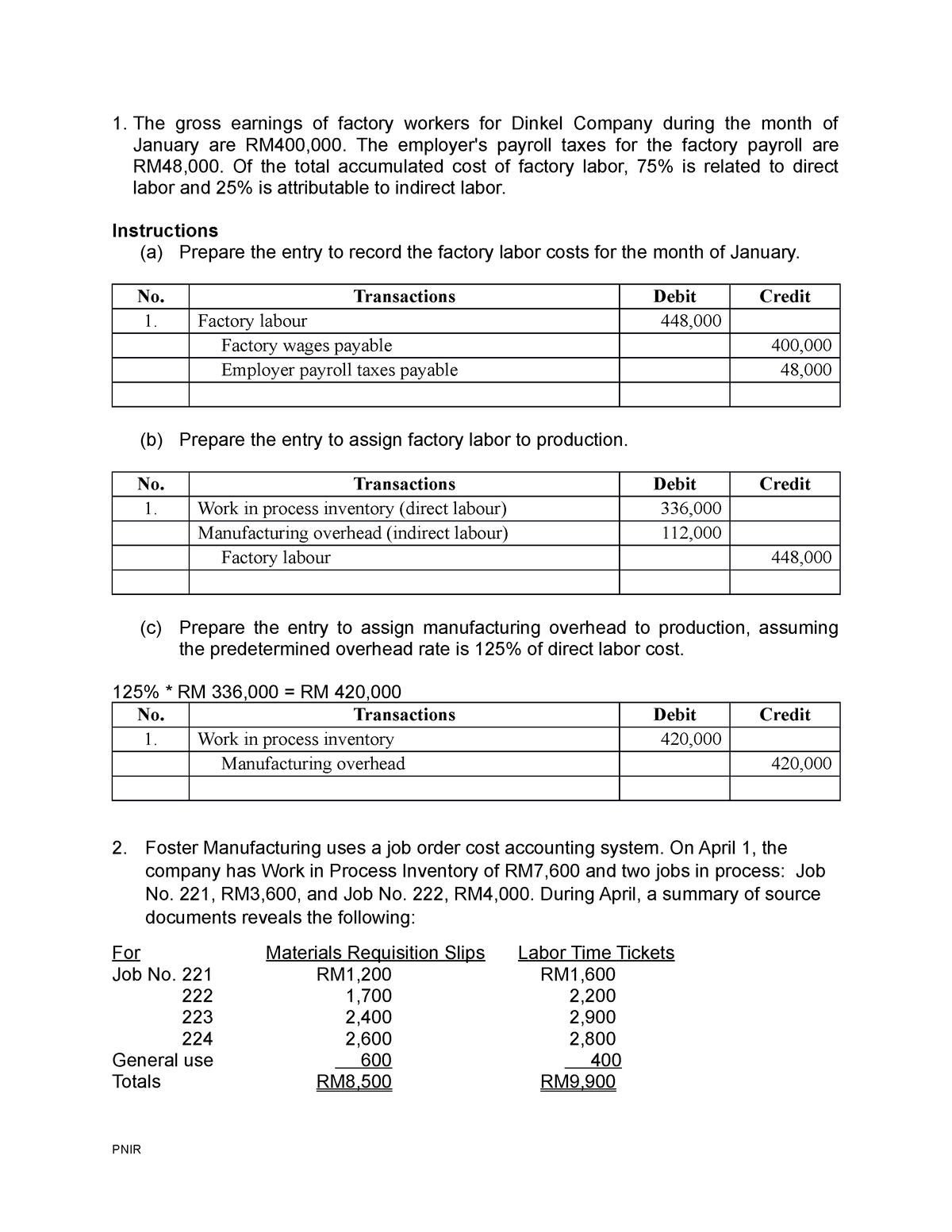

Then, these costs including the $20,000 of indirect labor will be transferred further to the working in process account using the predetermined overhead rates. In the job order costing, the labor cost of production during the period usually includes both direct labor cost and indirect labor cost. They are first transferred into manufacturing overhead and then allocated to work in process. The entry to record the indirect material is to debit manufacturing overhead and credit raw materials inventory. In addition to basic wages and salaries, an entity’s direct labor cost includes all costs and expenses needed to hire and keep direct labor workers in the organization. These costs and expenses take the form of relevant federal and state taxes, contributions and benefits provided by employers for the support and wellness of workers.

Direct Materials Requisitioned by the Shaping and Packaging Departments and Indirect Material Used

For example, hair stylists at a salon who perform haircuts and other services are considered direct labor while the maintenance staff and the receptionist who support them are indirect labor. Indirect labor refers to employees who are not involved in planning or construction projects. This includes human resources, administration, accountants, customers relations, etc. A standard hour is the number of production units which should be achieved by an experienced worker within a period of one hour. (1) Labour costs incurred are paid out of the bank before they are analysed further in the labour account.

The Balance Of Factory Overhead

Assume Creative Printers is a company run by agroup of students who use desktop publishing to produce specialtybooks and instruction manuals. Creative Printers uses job costing.Creative Printers keeps track of the time and materials (mostlypaper) used on each job. Unless overtime is worked at the specific request of a customer, overtime premium is part of the indirect labour costs of an organisation. Vienna is a direct labour employee who works a standard 35 hoursper week and is paid a basic rate of $12 per hour. The remaining hours are the total hours spent by one employee as indirect labor utilization. Since indirect labor cannot be traced back to a specific product or service, the related cost can’t be billed to the goods produced or the services rendered.

Ongoing Overapplied Overhead

If the applied overhead exceeds the actual amount incurred, overhead is said to be overapplied. This is usually viewed as a favorable outcome, because less has been spent than anticipated for the level of achieved production. Sometimes, in very specific cases, companies can do the same with salaries and wages. Just know that when they do, this is the final way labor can appear on the balance sheet electronic filing — as a capitalized expense. When production of the group exceedsthe standard – 200 pieces per hour – each employee in the group ispaid a bonus for the excess production in addition to wages at hourlyrates. A company operates a piecework system of remuneration, but alsoguarantees its employees 75% of a time-based rate of pay which is basedon $19 per hour for an eight hour working day.

Since this is an asset to asset transfer, we don’t make any changes to liabilities. Inventory is not just raw materials purchased and resold at a higher price. Instead, raw materials that the company purchases are “reworked” by employees before becoming sales, which allows them to be sold at a higher value.

Transferred Costs of Finished Goods from the Shaping Department to the Packaging Department

- We do this by debiting the WIP account and crediting the Wages payable account, as well as debiting the wages expense account.

- On the other hand, printing instruction manuals was quite profitable, so the company has focused more on the instruction manual market.

- A company operates a piecework system of remuneration, but alsoguarantees its employees 75% of a time-based rate of pay which is basedon $19 per hour for an eight hour working day.

- When we record a sale on the P&L, we list the indirect labor costs used to generate it on the P&L as well.

- In addition to these steps, we could also note that our accounts payable and wages payable liability accounts still have a balance of 51,500.

- Highly skilled and motivated workers exhibit enhanced efficiency and contribute towards controlling and reducing the total direct labor cost of the entity.

The importance of properly recording the production process is illustrated in this report on work in process inventory from InventoryOps.com. The preceding entry has the effect of reducing income for the excessive overhead expenditures. Only $90,000 was assigned directly to inventory and the remainder was charged to cost of goods sold.

For example, the company ABC, which is a manufacturing company, has incurred the direct labor cost of $45,000 and the indirect labor cost of $5,000 during the period. Of the total amount, $42,000 is related to the wages payable and the $8,000 is related to the payroll taxes payable. Notice, Job 105 has been moved from FinishedGoods Inventory since it was sold and is now reported as an expensecalled Cost of Goods Sold. Also, did you notice that actualoverhead came to $9,800 ($1,000 indirect materials + $2,000indirect labor + $6,800 other overhead from transaction g) but weapplied $9,850 in overhead to the jobs in transaction d? Wheneverwe use an estimate instead of actual numbers, it should be expectedthat an adjustment is needed. We will discuss the differencebetween actual and applied overhead and how we handle thedifferences in the next sections.

Amounts go into the account and are then transferred out to other accounts. At this point, we need to credit (decrease) inventory for every sale we make. This increases cash or accounts payable not only by the value of the inventory, but also by the margin we make on it. Now we have both raw materials and wages in our WIP account, which we then need to transfer to the inventory account as products are completed.

The journal entry to apply or assign overhead to the jobs would be to move the cost FROM overhead TO work in process inventory. Although you have seen the job order costing system using both T-accounts and job cost sheets, it is necessary to understand how these transactions are recorded in the company’s general ledger. In job order costing, the direct labor will be transferred to the working in progress account while the indirect labor will be transferred to the manufacturing overhead account. In the accounting of job order costing, the labor cost account is usually used for recording the labor cost that incurs during the period including both direct labor and indirect labor.

This is also a direct labour cost because the basic rate for overtime is part of the direct labour cost. It is the overtime premium which is usually part of the indirect labour cost. One of the most important distinctions of labour is between direct and indirect costs.

To best understand the specific journal entries related to inventory, as well as the relevant labor costs, let’s look at an example of a manufacturing company. The company assigns overhead to each job onthe basis of the machine-hours each job uses. Overhead is assignedto a job at the rate of $ 2 per machine-hour used on the job. Job16 had 875 machine-hours so we would charge overhead of $1,750 (850machine-hours x $2 per machine-hour). Job 17 had 4,050machine-hours so overhead would be $8,100 (4,050 machine-hours x$2).